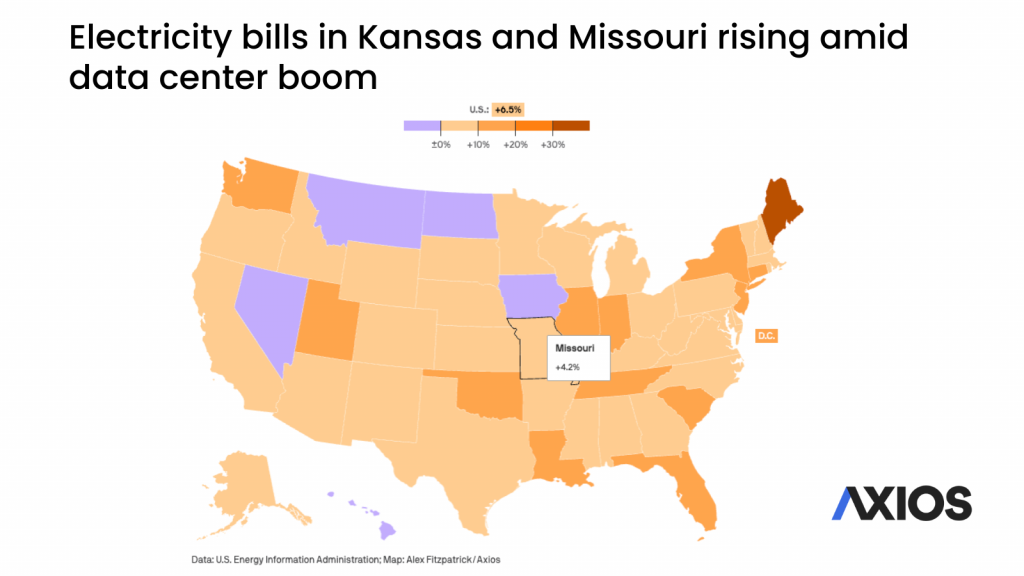

Missouri residents continue to speak out about the rising costs they are experiencing in their home electric bills. Within the past year, Missouri utility companies have averaged a four percent increase in the cost of the electricity they supply. Additionally, from 2020 to 2023, they experienced a collective rate increase of 20%. Consumers are noticing –– and they’re not happy.

In three weeks, an online petition that was launched in late July secured 3,000 signatures from Missouri residents who want to stop “excessive” rate increases by Ameren, the state’s largest utility.

One petitioner named Marissa wrote:

“Ameren has a monopoly on our electricity and it isn’t fair.”

She isn’t wrong. Missouri’s energy structure is vertically integrated, monopolized by the ratepayer-funded utility companies. This means the utility company controls the generation of electricity, the sale of the electric supply and the delivery of that product to your house. Without competition, it’s understandable to have the feeling of unfairness when you aren’t afforded any other options.

Missourians have also been expressing their frustration through the My Energy Choice campaign, a consumer advocacy campaign full of customers demanding state lawmakers take action to break up the utility monopoly. Melissa from Saint Joseph wrote:

“The current utility companies can charge whatever they want because they have no competition. I would love to be able to switch companies from these over-priced money hungry companies.”

This topic of utility monopolies was the focus of a recent article from KBIA, an NPR affiliate in Missouri. The authors of the article posed the question, Why are utility companies monopolies? The article includes perspectives from academics that riff on the idea that the mechanics of just one company monopolizing the power for a community is best to prevent various sets of poles and wires from attempting to deliver electricity. Another academic spoke to economies of scale and how utilities could produce cheaper electricity that would not occur if there was competition.

Unfortunately, this article or these experts did not address all the research or evaluate states with competitive markets, as there are 23 states that allow some or full electric competition.

THE DIFFERENCE BETWEEN MONOPOLY AND COMPETITIVE MARKETS

In a competitive market, utility companies still have an integral role in delivering electricity. There are not multiple sets of wires and poles for every supplier selling electricity. All power runs through the electric lines of the utility company, preventing energized spiderwebs on every street. A quick explainer can be found here.

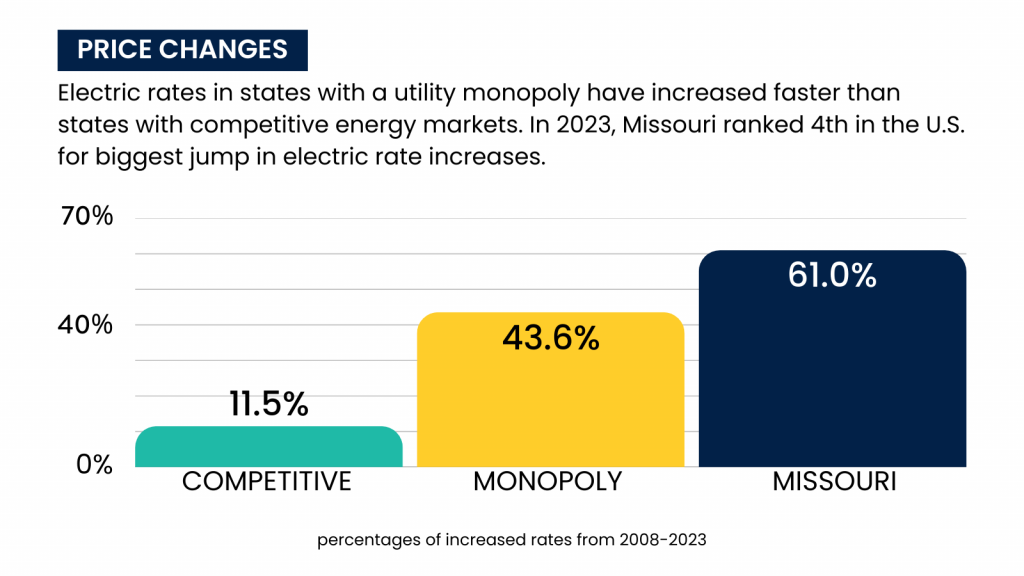

When it comes to price, like any product that has ever been sold, competition applies pressure to any seller with a compatible product to keep prices down. The same goes for electricity. The academics from the article mentioned above used Pennsylvania as an example of where competition has not worked for consumers, but a recent analysis of electric rates and retail supply offers conducted by a former Pennsylvania public utilities commissioner suggests otherwise.

SIMILARITIES BETWEEN TODAY’S MISSOURI AND ’90s PENNSYLVANIA

Pennsylvania was once like Missouri: a state with growing demand and not enough supply, high electric rates, power generation inefficiencies, a push to spend a lot of money on nuclear energy, plus occasional blackouts. This was the energy market in the early 1990s for the then-utility-monopolized Pennsylvania.

Knowing that a change needed to happen to protect consumers and ensure lights stayed on, state lawmakers passed legislation in 1996 that restructured Pennsylvania’s energy market, opening the doors for competition to generate and sell electricity. Nearly 30 years later, John Hanger, a Pennsylvania utility commissioner who was an architect for the Commonwealth’s market restructure, analyzed data to determine if the restructuring continues to be beneficial for consumers. The results speak for themselves.

PENNSYLVANIA CONSUMERS ARE BENEFITING FROM COMPETITION

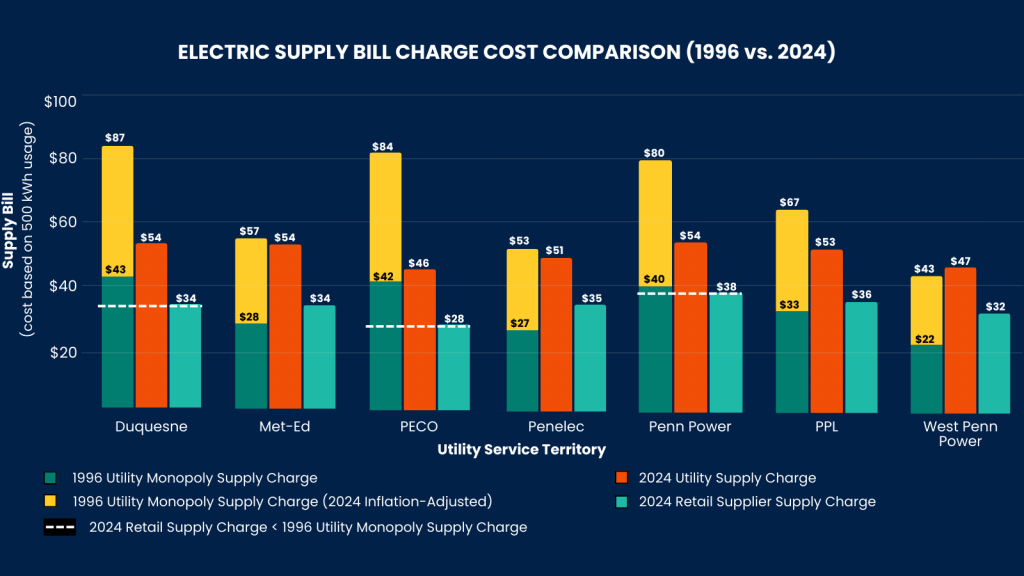

Hanger recently compared the Pennsylvania utility electric rates in 1996 from seven different service territories to the utility rates and retail supply offers from 2024 in those same territories. What he found is that customers could have enrolled with retail suppliers in 2024 at electricity prices that were cheaper than utility rates in 1996 –– direct comparisons, no adjustments. When inflation adjustments were added to the 1996 rates to conservatively estimate what they would equate to in 2024, Hanger discovered that the 2024 utility rates were cheaper than what they would have been projected to be based on the 1996 rates.

This demonstrates that price pressure from competition works.

Because Pennsylvania has competition, anyone selling electricity has to compete for the business of consumers. If prices don’t fall in line with other electricity products on the market, it’s less likely the consumer will purchase the product, opting for another product.

Pennsylvanians have robust options in the type of electricity they can purchase and in the length of their contracts. If a customer wants to purchase a premium product, such as 100% solar energy, they can do that. If they want to lock in a rate for 36 months without the worry of price volatility, they can do that too.

In Missouri, there are no alternatives and energy users are stuck with the prices that are set by the utility and Public Service Commission. The Consumers’ Council of Missouri reported that electric rates increased 20% from 2020 to 2023. That’s an annual cost increase of $327 for the average household. Data also shows that in 2023, Missouri ranked 4th in the country for the biggest jump in electricity, starting in 2008.

MISSOURIANS FORCED TO PAY FOR NEW POWER GENERATION

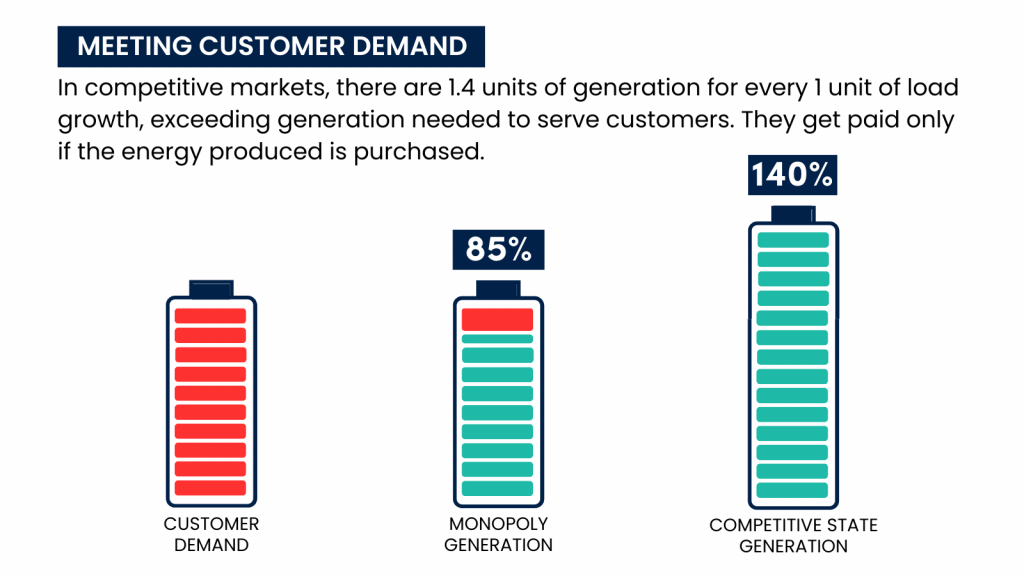

One of the biggest factors coming out of the restructuring is that Pennsylvania has built more baseload power plants and new power generation than Missouri and other nearby monopoly states –– and it happened without customers paying for it.

As a result of restructuring, competitive states have more power and better reliability than states that protected their utility monopolies. The new power generation projects in Pennsylvania are paid for by private investors with experience in producing energy from natural gas, wind, solar, hydro, nuclear, etc.

Unfortunately, in Missouri, all power generation is paid for by the ratepayers (customers). In fact, legislation (Senate Bill 4) was recently signed into law, allowing utility companies to bill for “construction work in progress” or CWIP, meaning before any energy is even produced –– let alone a shovel breaking ground –– the utility company can start billing ratepayers. And if priority projects are nuclear facilities, Missouri could find itself even closer to Pennsylvania’s position pre-1996.

This is a concern for Missourians who have voiced their displeasure, including a video of a petitioner on the Change.org campaign. A guy named Dewayne in a video message said:

“We have to build their power plants out of our pockets, and then have higher bills in the end of it all. And Ameren gets richer and we get poorer.”

PUTTING POWER IN THE HANDS OF THE PEOPLE

Missourians want to see change. They want to have a choice. And the state can help by putting the power in the hands of consumers to have some control over their electric bills.

The 2025 legislative session included legislation introduced by Sen. Nick Schroer and Rep. Don Mayhew to give electric customers energy choice. The companion bills, Senate Bill 487 and House Bill 417, were designed to create a competitive market, make suppliers earn the business of consumers, and invite privately invested power generation into the state to better support demand without forcing the ratepayers to fund those financially risky projects. Unfortunately for Missourians, those bills were heavily opposed by –– you guessed it –– the utility companies.

Consumers are sounding alarms as utility companies maintain total control. As petitions for change continue to swirl, perhaps Missourians will see energy choice legislation reintroduced in 2026.