Customers held captive by utility companies are demanding alternative solutions as electric rates increase

JEFFERSON CITY (Jan. 20, 2026) –– Sen. Nick Schroer (St. Charles County), Rep. Tricia Byrnes (St. Charles County) and Rep. Don Mayhew (Miller and Pulaski Counties) re-introduced legislation aimed at ending Missouri’s monopoly utility model. The bills create electricity options for residents and businesses, providing consumers more power over their electric bills. The Retail Energy Advancement League (REAL), a national advocacy organization dedicated to the expansion and modernization of American retail energy markets, applauds Schroer, Mayhew and Byrnes for their legislation.

“Missouri residents and businesses are in search of better options as they continue to be overwhelmed by their monthly electric bills,” said Chris Ercoli, president and CEO of the Retail Energy Advancement League. “Competition has proven successful in other states with better price performance, reliability and the variety of products and contract options available to commercial and residential customers. Sen. Schroer and Reps. Mayhew and Byrnes are taking action to address a problem facing all Missourians with a solution that can help move the state forward.”

The bills, Senate Bill 1411, House Bill 2233, and House Bill 2207 create a free-market alternative to a vertically integrated energy structure. Both bills require the electric utilities to compete with electricity generators and suppliers to build power plants and sell electricity. All electric users will benefit from having more options to power their homes and businesses.

Sen. Nick Schroer, SB 1411 sponsor

“As Americans, we have the freedom to shop for just about anything in this country, but in Missouri we don’t have the right to shop for our own electricity,” said bill sponsor Sen. Nick Schroer. “Missourians are trapped, held captive by a monopoly utility structure and the financial risks these investor-owned utilities place on the backs of their customers. This must change. Missourians deserve the right to hold utility companies accountable by having the ability to choose who supplies their electricity and what that energy product is, forcing all suppliers to compete for the business of consumers.”

Rep. Don Mayhew, HB 2233 sponsor

“My constituents keep adjusting their thermostats as utility companies continue to drive up electric bills,” said bill sponsor Rep. Don Mayhew. “Utilities can now bill for billion-dollar power plants before a shovel ever hits the ground — printing themselves sky-high guaranteed profits — while families are left wondering if they can even afford to keep the lights on. This legislation is long overdue and is needed to give Missourians real energy choices and hold utilities accountable in a consumer-first market.”

Rep. Tricia Byrnes, HB 2233 sponsor

“I continue to hear the outcry from my constituents about how expensive electricity is as they struggle with the fear of price gouging in a monopoly energy market,” said bill sponsor Rep. Tricia Byrnes. “My colleagues Sen. Schroer and Rep. Mayhew gained traction last year with legislation to break up the monopoly market and give consumers energy choices. By introducing House Bill 2233, I’m helping to carry that momentum forward to help give consumers a stronger voice –– and options –– to hold utility companies more accountable.”

Large energy users and industry organizations have previously testified in strong support of the legislation to help reduce the cost of electricity and ensure energy reliability. A representative of the auto manufacturer Ford Motor Company, which employs more than 9,000 workers at its Claycomo, Missouri plant, pointed to the successes of Ford plants in other states that have introduced competitive energy options.

Testimony from Tony Reinhart, director of government relations for Ford Motor Company

“Our utility rates have become one of our largest cost challenges with no real ability to offset those increasing costs. … Missouri doesn’t normally look to Illinois for good public policy. But Illinois got it right where they have unbundled generation, transmission and distribution services in a fair and equitable manner, providing us the ability to purchase power on the open market and better manage our costs.”

BACKGROUND ON MISSOURI ENERGY MARKET

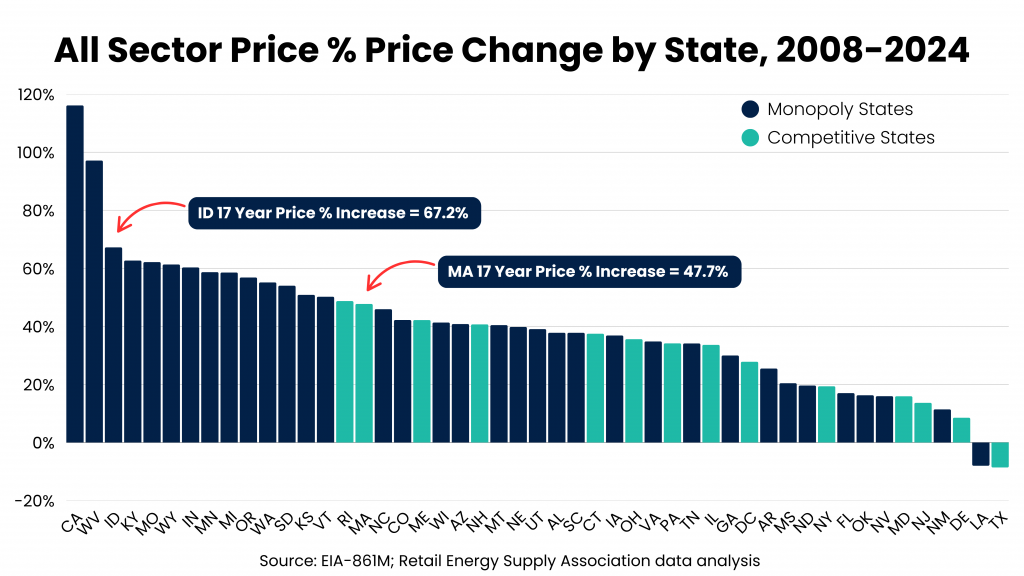

- Missouri ranks 5th worst among all states in price percentage change from 2008-2023, with an increase of 61% during that time

- Residential electric rates increased by 20% from 2020-2023, according to Consumers Council of Missouri

- Missouri is a net importer of electricity

- The state consumes 8x more energy than its utility companies produce

- Missouri utility companies have only built or updated ~2,000 megawatts (MW) of power generation from 2008-2023

- With the construction work in progress (CWIP) law, utilities can plan to build muli-million dollar power plants to increase generation and bill customers for those costs before construction even begins

- The Missouri Public Service Commission unanimously approved new rates for large electric users like data centers even after concerns were raised about increases to residential electric bills

MISSOURIANS ARE SPEAKING OUT

Missouri residents statewide are voicing opposition to the utility monopoly model and the need for choices.

“Unleash the free market that encourages companies to be innovative, compete for their customers’ business, provide return on investment, and offer respectful customer service. Had there been electric company competition, maybe Ameren wouldn’t have been so heavy.” -Mary Ann B., St. Peters

“Ameren has gone up nearly 40%. They want us to pay for future infrastructure, while banking OUR MONEY gaining THEM INTEREST!” -Lori W., Wentzville

“I hate the fact that I do not have a choice in who my utility company is. The only one available in my county is Ameren, and my average bill is $400 a month, with up to $900 during the summer months. This is a marked increase over even last year. How is anyone supposed to afford this?” -Rebecca S., Moberly

“Energy costs are much too high. Every time Evergy requests an increase in electric rates they always get what they ask for.” -Kristine S., Belton

“Evergy is monopolizing the entire two-state area. They overcharge and tack on all kinds of different fees. People deserve to have a choice on who their energy provider is.” -Melanie J., Kansas City

“It’s awful and killing our town. We have lost so many businesses this year because they can’t afford to operate under Liberty Utilities.” -Jacquelynn R., Bolivar